Download the accompanying IPython Notebook for this Tutorial from Github.

Last Tutorial, we outlined steps for calculating the Stochastic Oscillator.

In this Tutorial, we walk through calculating 5-day, 10-day, and 20-day future returns, from historical data.

Caculating 5-day, 10-day, and 20-day future returns will allow us to identify relationships between current technical indicators and future returns.

Let’s use Python to compute the 5-day, 10-day, and 20-day future returns.

1.) Import modules.

import pandas as pd

import numpy as np

from pandas_datareader import data as web

import matplotlib.pyplot as plt

%matplotlib inline2.) Define function for querying daily close.

def get_stock(stock,start,end):

return web.DataReader(stock,'google',start,end)['Close']3.) Define function for calculating the 5-day future return.

def fiveday(close):

fiveday = ((close.shift(-5) - close) / close) * 100

return fiveday4.) Define function for calculating 10-day future return.

def tenday(close):

tenday = ((close.shift(-10) - close) / close) * 100

return tenday5.) Define function for calculating 20-day future return.

def twentyday(close):

twentyday = ((close.shift(-20) - close) / close) * 100

return twentyday6.) Query daily close.

df = pd.DataFrame(get_stock('FB', '1/1/2016', '12/31/2016'))7.) Run daily close through fiveday, tenday, and twentday functions. Save series to new columns in dataframe.

df['5 day'] = fiveday(df['Close'])

df['10 day'] = tenday(df['Close'])

df['20 day'] = twentyday(df['Close'])

df = df.dropna()

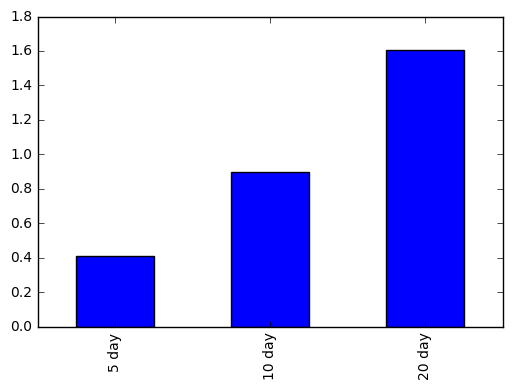

df.tail()8.) Plot average 5-day, 10-day, and 20-day future returns.

df2 = df[['5 day', '10 day', '20 day']].mean()

df2.plot(kind='bar')

There you have it! We calculated 5-day, 10-day, and 20-day future returns. Here’s the full code:

import pandas as pd

import numpy as np

from pandas_datareader import data as web

import matplotlib.pyplot as plt

%matplotlib inline

def get_stock(stock,start,end):

return web.DataReader(stock,'google',start,end)['Close']

def fiveday(close):

fiveday = ((close.shift(-5) - close) / close) * 100

return fiveday

def tenday(close):

tenday = ((close.shift(-10) - close) / close) * 100

return tenday

def twentyday(close):

twentyday = ((close.shift(-20) - close) / close) * 100

return twentyday

df = pd.DataFrame(get_stock('FB', '1/1/2016', '12/31/2016'))

df['5 day'] = fiveday(df['Close'])

df['10 day'] = tenday(df['Close'])

df['20 day'] = twentyday(df['Close'])

df = df.dropna()

df.tail()